VICTOR ANASIMIV

I am a top-ranking mortgage broker with Dominion Lending Centres, Modern Mortgage Group, in the Comox Valley. My goal is to make the mortgage process as seamless and stress-free as possible for my clients. Since I started mortgage brokering in 2008, my focus has been on honest, open communication and delivering outstanding customer service; because I believe in putting my clients’ needs first.

As a long-time resident of the Comox Valley, I have in-depth knowledge of the local market and am actively involved in my community. While my primary focus is helping clients on Vancouver Island, I also assist people across Canada with their mortgage needs. No matter where you are, I’m committed to helping you secure the best financing solutions.

Having personally purchased multiple properties, I understand that purchasing real estate is an exciting and sometimes stressful journey. That’s where I come in; whether it is a purchase or a mortgage refinance, I help simplify the process, answer all your questions, and guide you through every step with confidence.

I can help you by:

- Finding you the right mortgage options that fit your specific financial goals and situation

- Accessing a wide network of lenders, including big banks, small credit unions, and specialty trust companies, to get you the best rates and terms

- Explaining complex mortgage details in clear, straightforward language

- Managing the entire application process efficiently, saving you time and stress

You've got a busy life; relax and let me be your personal mortgage shopper.

Understanding mortgage financing can be difficult, it doesn't have to be. Here's the plan!

Connect directly

The process starts when you get in touch. Let's take a look at your financial situation and put together a plan to

find the best mortgage for you!

Discuss your options

When it comes to mortgage financing, you have options! Let's clarify those options, so you can make the decision that best suits your needs.

Arrange the paperwork

Paperwork is the nitty gritty of mortgage financing. Let's make sure you know exactly what is required of you at every step, limiting any delays.

Lifetime support

As long as you need a mortgage, be assured that you'll receive ongoing professional mortgage advice. Connect anytime!

I can help you arrange mortgage financing for the following services:

Lenders

I've developed excellent relationships with many lenders across the country.

Let's figure out which one has the best product for you.

Mortgage Articles

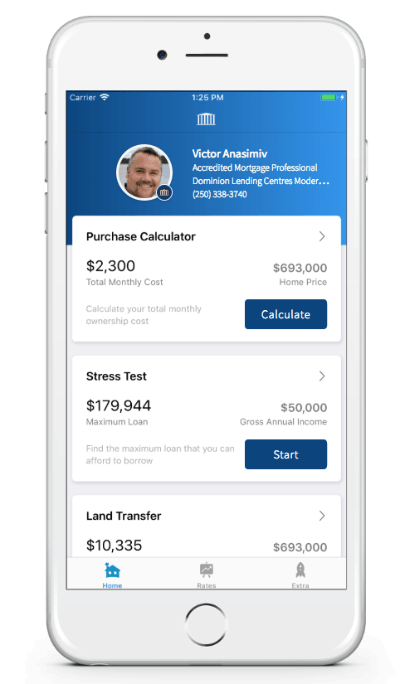

Download My Mortgage Toolbox

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese